Value triumphs Momentum in FY’24 from the quant lens

- Share.Market

- 4 min read

- 15 Apr 2024

By Share.Market Research

FY’24 was quite the rollercoaster ride, filled with geopolitical tensions, and big corporate shake-ups. From state elections in three states, preparations for the 2024 general election, high-impact geopolitical events, the Red Sea crisis, and corporate events like the HDFC-HDFC Bank merger, the markets could not have been more unpredictable.

Despite all this chaos, the Nifty 500 managed to pull off an impressive return of around 40.5%, which is pretty outstanding. The performance was even better for mid and small-cap indices. However, as a quant-powered stockbroker equipped with an intelligence layer of factor-based analysis, we wanted to delve deeper into the financial year gone by from a quantitative lens. Here’s what we found.

Value made a comeback!

Note: Risk-adjusted returns are factual, shown for information purposes only, and not as an advertisement/promotion or as an assurance of future returns. Past performance does not guarantee future returns.

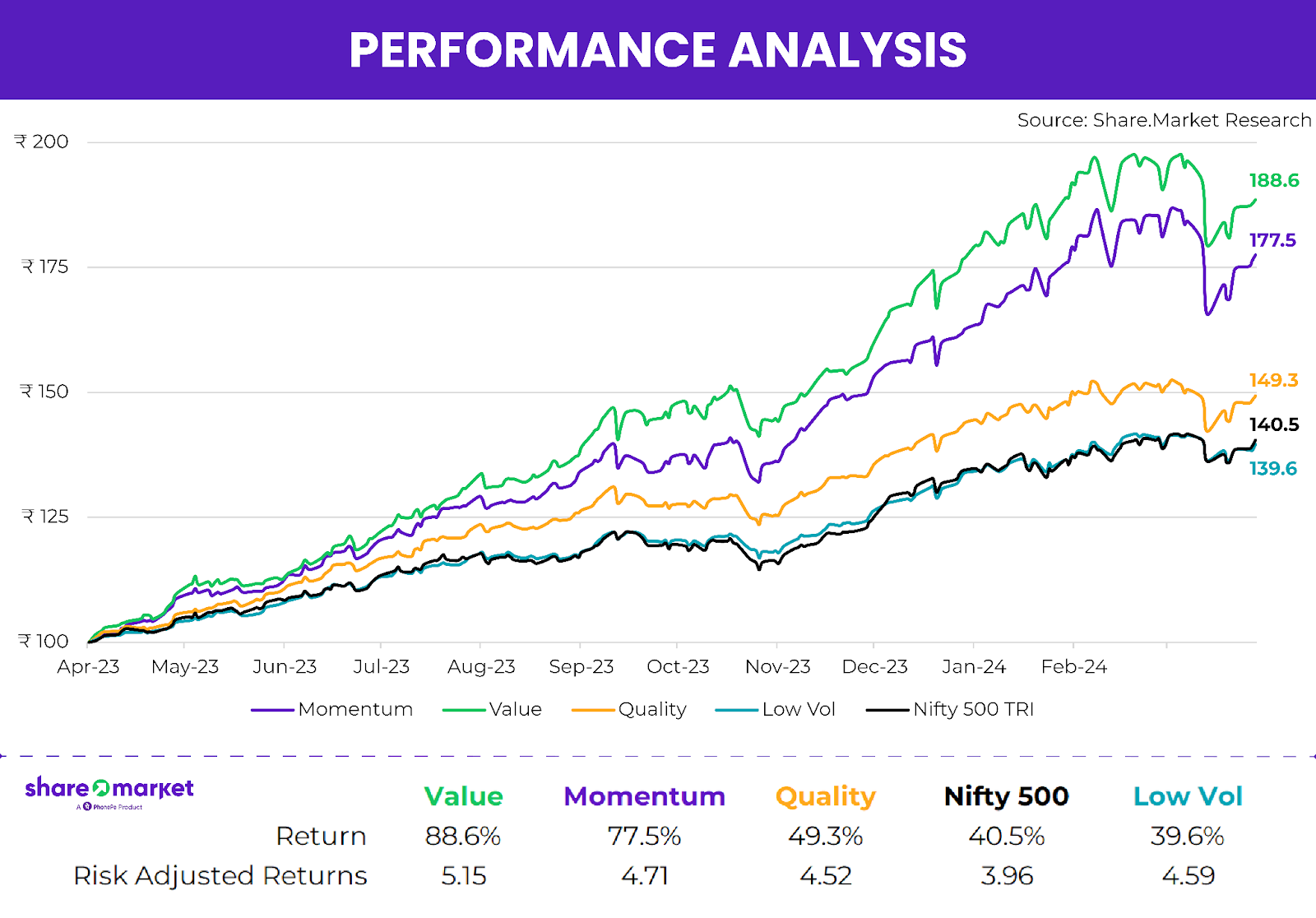

In our factor universe, if we put our proprietary Momentum, Value, Quality, and Low Vol portfolios head to head against NIfty 500 TRI, they all outperformed the latter significantly, except Low Vol. If we look at risk-adjusted returns, our Low Vol portfolio too, did not disappoint. While one year’s performance in isolation isn’t necessarily indicative of the soundness of the signals we employ in our research, it validates our ongoing thesis.

A refreshing observation was the comeback made by the Value factor in FY’24. In recent years, particularly since COVID, Momentum had consistently led market returns, while Value struggled to catch up. Finally, FY’24 marked the year when the tables turned, and Value outperformed Momentum.

This wasn’t too surprising, especially considering the stellar performance of PSU stocks during this period. The rally in Nifty PSU made it one of the top-performing indices of the year, and PSU stocks have always scored high on Value metrics due to their tendency to trade at lower valuations. Well, not anymore! A rally in PSU stocks explains the outsized returns of our Value portfolios.

Another thing to note is how Value and Quality factors tend to have longer cycles than Momentum. While Momentum relies more on price-based signals, Value and Quality factors dig deeper into business fundamentals. So, even though they might not always be in the limelight, they usually come back swinging when their time comes. Value has come back after a long time, but has its time come – we surely don’t know.

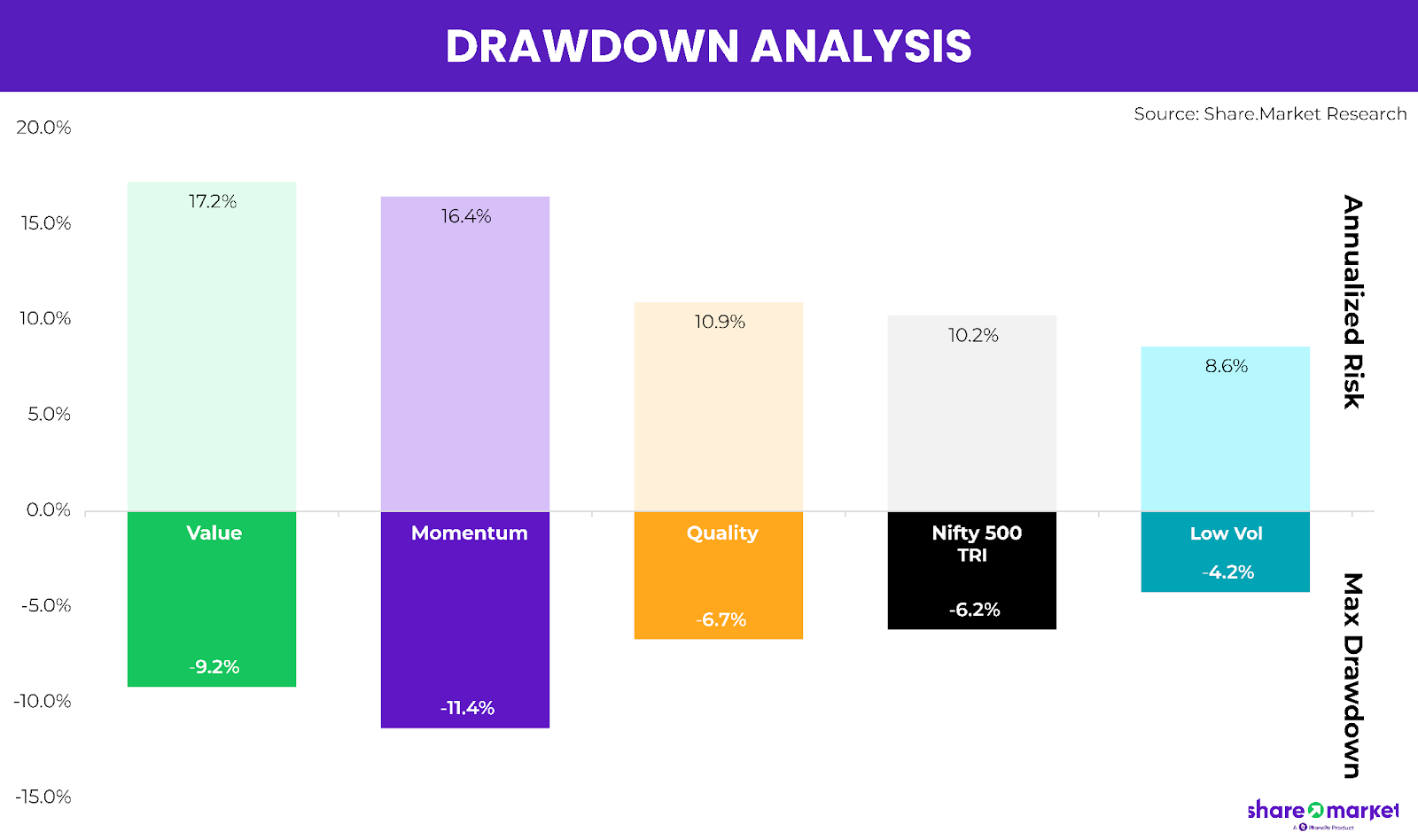

Let’s not forget risk

Turning our attention to drawdowns, we observed textbook examples of how different factors fared. Momentum experienced the highest drawdowns, while Low Vol lived up to its name by exhibiting lower drawdowns. Value and Quality factors fell between these two extremes.

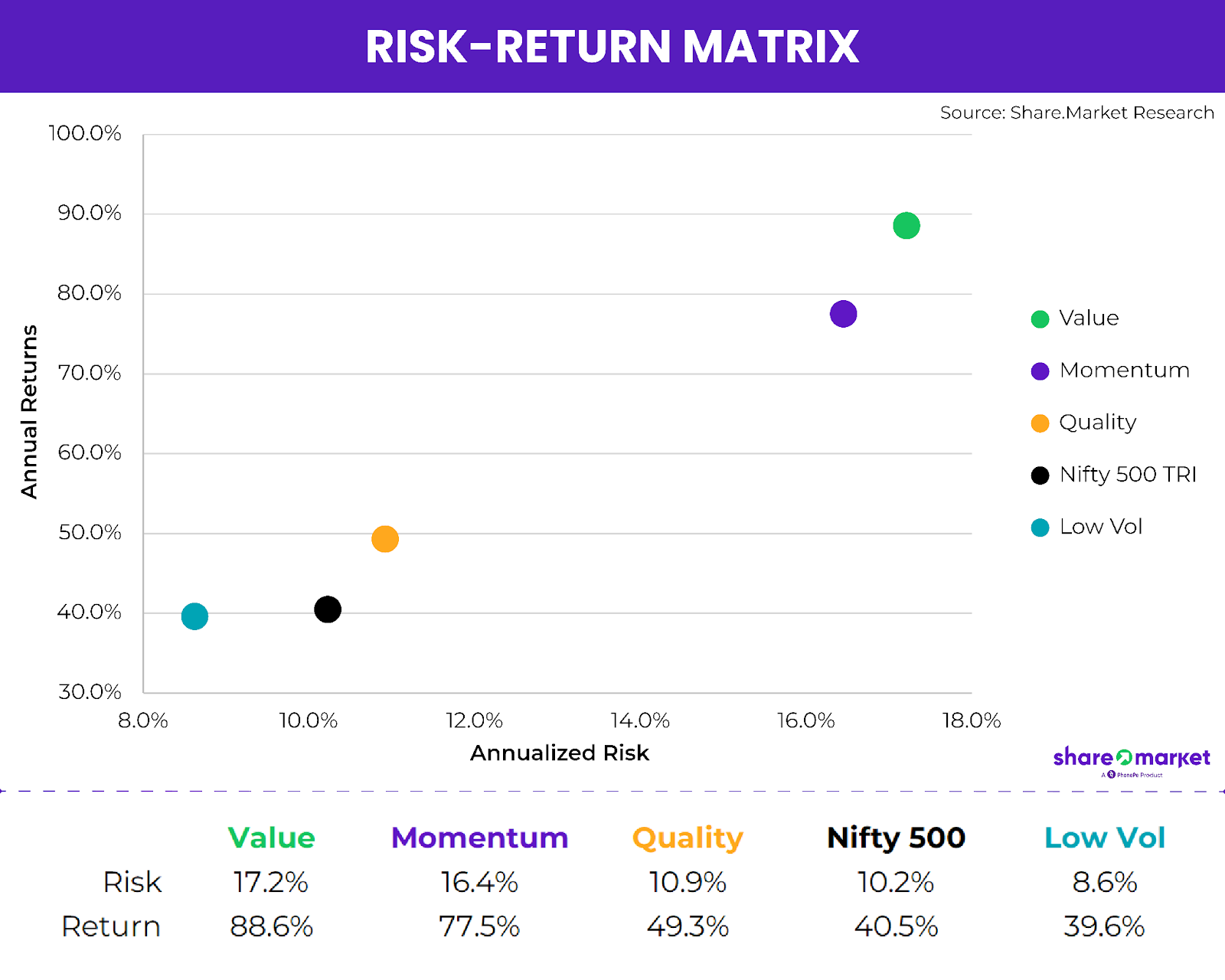

Constructing a risk-return matrix, we witnessed the academic theory playing out, where assuming higher annualized risk was rewarded with higher returns. This graph aids investors in understanding which factors they should consider while constructing their portfolios, taking into account the level of risk they’re willing to assume and the returns they expect. There’s no one-size-fits-all factor, and diversity in approach is key.

Concluding

This study helped us solidify our conviction of using factor-based analysis in India to provide better investment products to investors than vanilla passive options. If you are an investor looking to add exposure to different factors in your portfolio, you are way ahead of the general investing populace, and this can play in your favor, as we have already seen panned out in Western nations where factor-based investing is finally mainstream. Until then, in math & machine we trust.

This article was originally published in Economic Times on 14-04-2024

Disclaimer

Investments in securities are subject to market risks. Read all the related documents carefully before investing.

All investors are advised to conduct their own independent research into investment strategies before making an investment decision. Past performance does not guarantee future returns.

PhonePeWealth Broking Private Limited is a member of NSE & BSE with SEBI Regn. No.: INZ000302639, Registered Office Address: Office – 2, Floor 3, Wing A, Block A, Salarpuria Softzone, Bellandur Village, Varthur Hobli, Outer Ring Road, Bangalore South, Bangalore, Karnataka – 560103, Depository Participant of CDSL Depository with SEBI Regn. No.: IN-DP-696-2022, Research Analyst– INH000013387 and ARN- 187821. Member id: BSE – 6756 NSE 90226. CIN U65990KA2021PTC146954.

Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

This article is for educational purposes and should not be considered as a recommendation.