Do Value Funds Truly Hold Value? Answering The Question From Factor Lens

- Sujit Modi

- 6 min read

- 12 Feb 2024

By Share.Market (PhonePe Wealth) Research

Introduction

As factor investing gains ground in India, index providers like NSE roll out sophisticated “strategy indices” based on Momentum, Quality, Value, and Alpha. Despite this, our mutual fund industry lags in providing passive options. Currently, a limited number of ETFs and mutual funds cater to these strategies.

So we are still yet to catch up, but the mutual fund industry did compensate for the lack of products in factor space by having a dedicated category of mutual funds called “Value Funds.”

Value Funds are designed to spot undervalued stocks poised for future success, aligning with the principles of the “value factor.” It is a viable alternative for investors seeking value factor in their portfolios.

As Share.Market Research, which powers Intelligence for Investors and Traders, we wanted to know how much “value” these value funds have or if it is a product of marketing strategies. Let’s dive into our findings.

But, What Defines Value in Investing?

As mentioned, the Value factor seeks out stocks that appear attractively priced compared to their fundamentals. In simpler terms, it hunts for stocks that hold more value than what their market price might suggest.

But how to measure Value? Pinning down a universal definition for Value isn’t straightforward. Investors employ various accounting metrics like Earnings, Book Value, Revenue, Dividend etc. or a blend of these to determine a stock’s value relative to its price.

Here’s where it gets interesting. These accounting metrics were designed to meet the book-keeping requirements of the business. They were never meant to be used for valuation, which falls within the realm of cash flows. Accounting metrics are based on numerous accounting estimates prone to estimation errors.

However, cash flows have their own set of issues. There are numerous definitions of cash flow: Operating Cash Flow, Free Cash Flow, Free Cash Flow to Firm Vs Equity. Which one to use? Also, it can be volatile due to CapEx’s expectations of the business or economic cycle to which a particular industry is exposed.

At Share.Market Research, we combine Cash Flow and Earnings using a balanced approach to Value Factor. Cash Flow and Earnings definitions are arrived at after backtesting multiple variations over the last decade. This hybrid approach allows us to define Value, assign value scores to stocks, ETFs, and MFs, and subsequently rank these assets based on the value factor.

These value scores and rankings serve as our toolkit in answering the fundamental question at the heart of this research – Do Value Funds genuinely live up to their name?

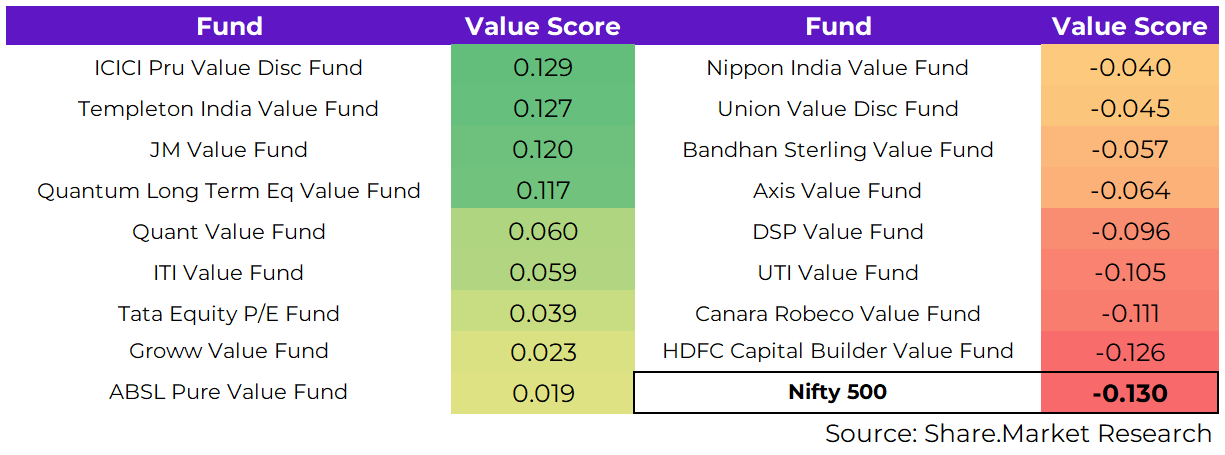

Note: We chose 17 mutual funds categorized as Value Funds for this study. The factor scores and returns discussed below pertain to the period from January 2, 2023, to January 15, 2024. Direct growth options of the schemes have been chosen for return calculations.

How do Value Funds compare to Nifty 500?

When we computed the average Value score of 17 mutual funds against the Value score of Nifty 500 over the specified period, an expected revelation unfolded.

Every single fund boasted a higher score relative to the benchmark. In simple terms, these Value funds were genuinely packed with more value than the broader Nifty 500.

Now, let’s talk about academic theories. They tell us that a value tilt could potentially translate to outperformance.

Well, in our study, the correlation isn’t as straightforward.

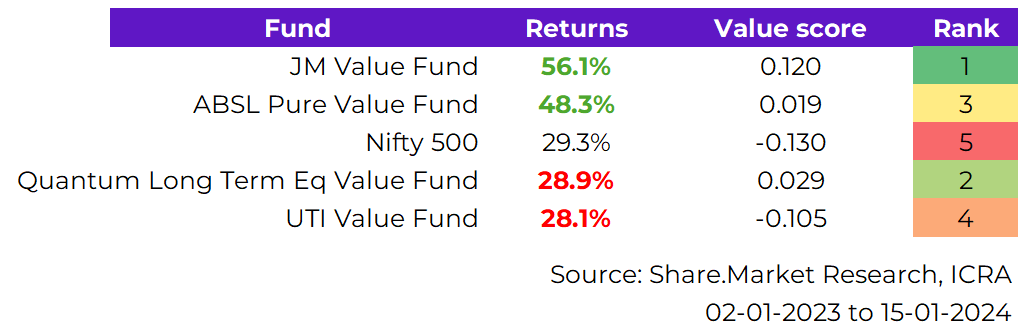

Surprisingly, when we picked the two extremes – the best and worst-performing funds during the period – and compared their Value scores, we stumbled upon an unexpected twist.

Based on total returns, the second-worst performing fund (ranked 2 in the above table) flaunts a higher Value score than its second-best performing counterpart (ranked 3 in the above table). Data don’t lie, and this revelation challenges conventional wisdom.

What can we infer from it? Value alone is not responsible for returns in Value funds. There are more mystic forces at play that might better explain what is happening.

Enters Momentum

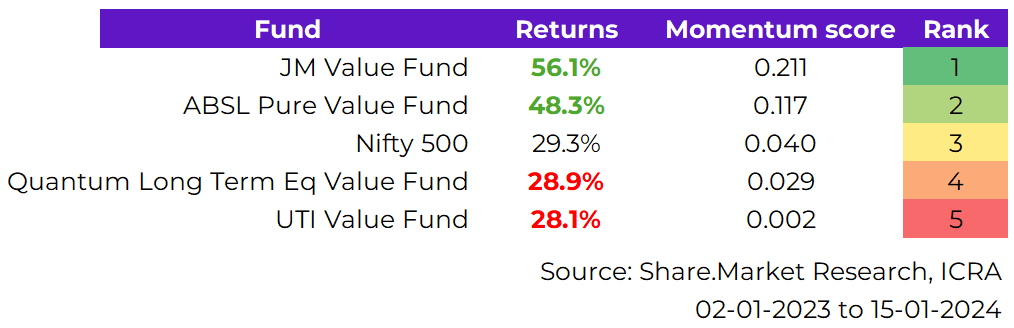

When Value did a poor job explaining and understanding what made Value funds deliver performance, we turned to a more reliable factor in the Indian markets – Momentum.

Momentum highlights the tendency of winning stocks to continue performing well in the near term.

So, we crunched the numbers, computed Momentum scores for our funds, and voila!

We observed as fund returns dipped, their Momentum scores followed suit, creating a clear correlation. Interestingly, Momentum turned out to be a more straightforward storyteller when it came to explaining the returns of Value funds.

Take, for instance, the ICICI Prudential Value Discovery Fund, which scored the highest value score but ranked 13/17 in terms of returns because of its low momentum score.

What can we conclude?

In wrapping up our study on Value Funds, the verdict is clear. Yes, Value funds generally outperform the market thanks to their value tilt. However, the real game-changer lies in understanding the sequence of returns.

Here’s the gist – the performance of these funds aligns more with their exposure to the momentum factor than their pure value orientation.

Relying solely on the value factor might not be the wisest move for those eyeing consistent outperformance.

The winning strategy? Combine the forces of the Value and Momentum factors. This strategic alliance holds the key to maximizing the benefits of factor investing in your portfolio.

Disclaimer:

“Mutual Fund investments are subject to market risks, read all scheme-related documents carefully.”

Investments in securities are subject to market risks. Read all the related documents carefully before investing. All investors are advised to conduct their own independent research into investment strategies before making an investment decision.

PhonePeWealth Broking Private Limited is a member of NSE & BSE with SEBI Regn. No.: INZ000302639, Registered Office Address: Office – 2, Floor 3, Wing A, Block A, Salarpuria Softzone, Bellandur Village, Varthur Hobli, Outer Ring Road, Bangalore South, Bangalore, Karnataka – 560103, Depository Participant of CDSL Depository with SEBI Regn. No.: IN-DP-696-2022, Research Analyst– INH000013387 and ARN- 187821. Member id : BSE – 6756 NSE 90226. CIN U65990KA2021PTC146954. Registration granted by SEBI, and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

This article is for educational purposes and can not be considered as a recommendation.