Soaring High: A Look at India’s Thriving Airline Sector

- Share.Market

- 6 min read

- 04 Jun 2024

India’s airline industry is experiencing rapid growth, driven by a growing middle class and a boom in the travel market. This analysis provides a comprehensive overview of the sector, including airports, airlines, on-ground services, and recent developments.

Overview of the Indian Aviation Sector

The Indian Aviation industry will have a market size of USD13.89 billion in 2024 and is expected to grow at a CAGR of 11.08% and reach a market size of USD26.08 billion by 2030. By this time India is expected to become the third-largest air passenger market globally, overtaking China and the United States stated by the International Air Transport Association (IATA).

The demand for air travel in India is increasing, leading to more planes operating in the sector, which is set to reach 1,100 planes by 2027. From April 2023 to January 2024, domestic passenger traffic rose by 15.3% to 254.44 million, and international passenger traffic increased by 23.5% to 57.57 million compared to the same period last year. In FY23, Indian airports projected domestic passenger traffic to hit 270.34 million (up 62.1% YoY) and international traffic to reach 56.9 million (up 157% YoY) compared to FY22 as per the report by IBEF.

Freight traffic grew at a CAGR of 2.20% from 2.70 MMT to 3.15 MMT between FY16 and FY23, with a potential to reach 17 MT by FY40. In FY22, there were 1.75 million aircraft movements, increasing to 2.5 million in FY23. To accommodate rising air traffic, the Indian government plans to increase operational airports from 148 in 2023 to 220 by 2025.

A Look at the Value Chain

The Indian airline sector functions smoothly, with various players working together. Here’s a breakdown of the key components:

Aircraft Manufacturers: Global giants like Airbus and Boeing supply aeroplanes to Indian airlines.

Airports: Government and private entities manage airports, providing infrastructure for take-off, landing, and passenger services.

Airlines: Passenger carriers like IndiGo and SpiceJet offer domestic and international flight services. They lease or buy aircraft and manage ticketing, crew, and in-flight services.

Ground Handling Services: Companies like Celebi and Swissport provide ground support for airlines, including baggage handling, cargo management, and aircraft cleaning.

Quick Service Restaurants (QSRs): Food outlets like McDonald’s and KFC cater to passengers at airports, offering convenient dining options.

Duty-Free Shops: These shops at airports allow passengers to purchase products like liquor, cosmetics, and souvenirs without paying customs duties.

Regulatory Bodies: The Directorate General of Civil Aviation (DGCA) governs safety standards and licensing for airlines and airports.

Listed Indian Companies

| Company | Market Cap (Rs Crore) on 29/04/2024 | Revenue (Rs Crore) | Net profit (Rs Crore) | Debt-to-Equity Ratio | Industry |

| GMR Airports Infrastructure | 54,891 | 6693 | -840 | 2.1 | Airports |

| Nestle India Ltd. | 239497 | 19126 | 2999 | 0.1 | QSR (Food & Beverages) |

| Jubilant FoodWorks Ltd. (Dominos Franchise) | 28,082 | 5158 | 353 | 1.25 | QSR (Restaurants) |

| Shoppers Stop Ltd. | 7,799 | 4022 | 116 | 10.54 | Duty-Free Retail |

| IndiGo (InterGlobe Aviation Ltd.) | 152,408 | 54446 | -317 | – | Airline |

| SpiceJet Ltd. | 4,832 | 8874 | -1513 | – | Airline |

The companies in the airline industry are highly impacted by their interest cost because most of the airlines operate on lease. The depreciation cost and interest cost significantly affected their net margins. GMR airport infrastructure company is the only company which is listed in managing the airports.

In 2022, IndiGo captured the market with nearly 55% of the market share at the end of the year. Vistara and Air India both have a market share of 9.2% each, followed by SpiceJet and AIX Connect (AirAsia India) with 7.6% each. Go First had a share of 7.5%, and Akasa Air finished the year with 2.3%.

IndiGo bought 30 A350-900 planes from Airbus for USD 4-5 billion, Air India’s order is for 470 planes which includes 250 from Airbus, and 220 from Boeing worth USD 70 billion, IndiGo’s previous record order was valued at USD 55 billion, and Akasa Air’s order is worth USD 20 billion for 150 Boeing 737 MAX planes. Indian carriers collectively ordered 1150 planes in 15 months, with 1590 including purchase rights.

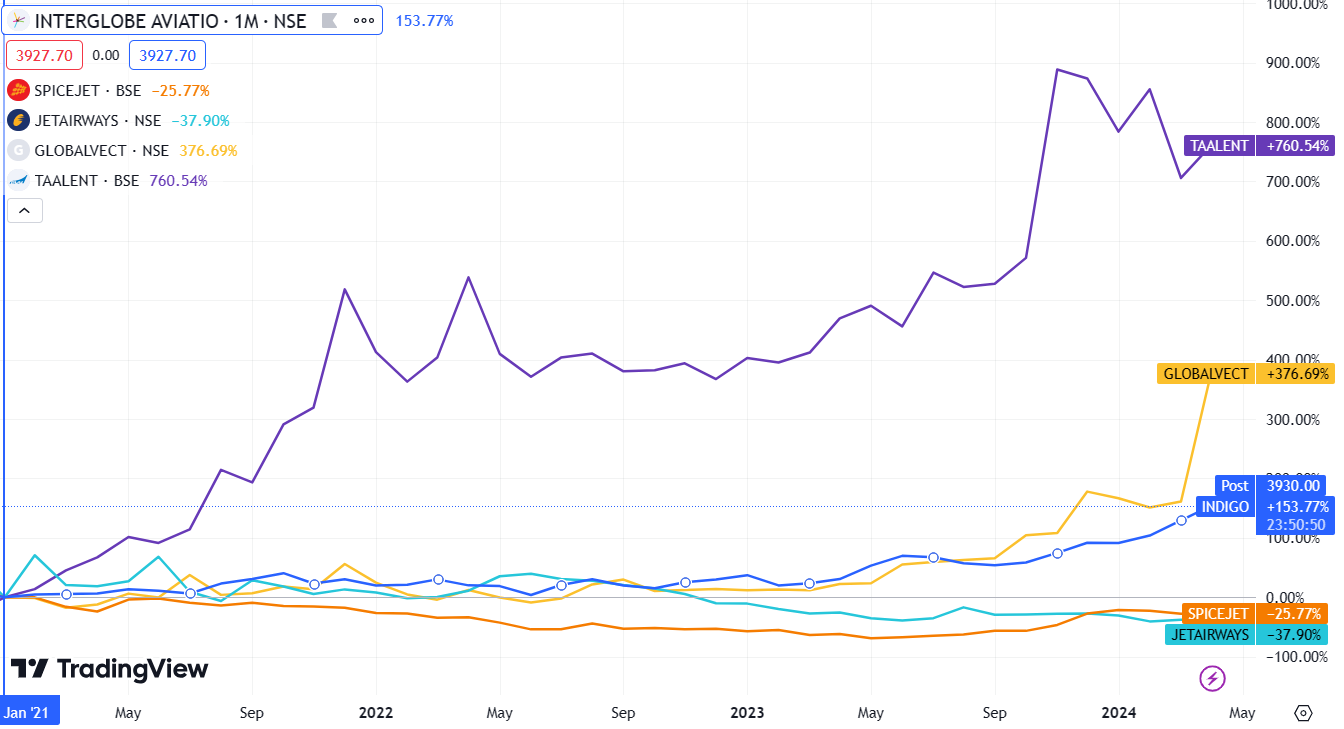

Performance of airline stocks post-pandemic

Post-COVID, Taal Enterprise and Global Vectra Helicorp have significantly outperformed other airline stocks as both companies operate in charter services. The companies operate only for a limited segment of people.

Understanding the Growth Trajectory

Passenger Traffic: Domestic passenger traffic doubled from 60 million in 2014 to 143 million in 2020 (pre-pandemic). International passengers also saw a significant rise from 43 million to 64 million during the same period.

Fleet Size: Despite the pandemic, the number of aircraft in India has increased from around 400 in 2014 to 723 in 2023 and to increase by 1100 by 2027.

Airports: India has a vast network of 149 operational airports which includes 137 airports, 2 water aerodromes and 9 Heliports. Among these 29 are international, 92 are domestic and 10 are custom airports. Under the UDAN scheme government aims to develop 100 airports by 2024, 2.15 lakh UDAN flights have been operated, and 11 million passengers have availed of benefits under the UDAN Scheme.

List of India’s Top 5 Busiest Airports

| Rank | Airport Name | State | Number of passengers handled in 2023 (in millions) | Managed By |

| 1 | Indira Gandhi International Airport (Delhi) | Delhi | 65.33 | Delhi International Airport Limited (DIAL) |

| 2 | Chhatrapati Shivaji Maharaj International Airport (Mumbai) | Maharashtra | 43.93 | Mumbai International Airport Limited (MIAL) |

| 3 | Kempegowda International Airport (Bengaluru) | Karnataka | 31.91 | Bangalore International Airport Limited (BIAL) |

| 4 | Rajiv Gandhi International Airport (Hyderabad) | Telangana | 21 | GMR Hyderabad International Airport Limited (GHIAL) |

| 5 | Chennai International Airport (Chennai) | Tamil Nadu | 18.57 | Airports Authority of India (AAI) |

Recent Updates

Government Reforms: The government is focusing on improving airport infrastructure and introducing policies to make air travel more affordable. In April 2020, the GST on MRO (Maintenance, Repair and operation) was reduced from 18% to 5%. This includes initiatives like the UDAN (Ude Desh Ka Aam Nagrik) scheme, which aims to connect smaller cities with air services.

Consolidation: The industry is witnessing some consolidation, with talks of mergers and acquisitions between airlines. This could lead to a more streamlined market with fewer players.

Focus on Sustainability: Airlines are becoming increasingly aware of their environmental impact and are exploring ways to reduce carbon emissions. This includes using fuel-efficient aircraft and adopting sustainable practices.

Challenges and Opportunities

The sector faces challenges:

Fuel Price Fluctuations: Rising fuel prices can significantly impact airline profitability.

High Operating Costs: Factors like airport charges and staff salaries contribute to high operational costs for airlines.

Competition: The Indian aviation market is highly competitive, with low-cost carriers putting pressure on pricing.

Significant opportunities exist:

Growing Middle Class: As India’s middle class expands, demand for air travel is expected to rise further.

Untapped Markets: Tier-2 and Tier-3 cities have immense potential for air travel growth, with the UDAN scheme playing a key role.

M&A Activity: Consolidation can lead to a more efficient market and improved profitability for airlines.

Conclusion

The Indian airline sector is on an upward trajectory, driven by a growing economy and a rising middle class. While challenges exist, the government’s focus on infrastructure development and policy reforms paints a positive picture. With a focus on sustainability and cost control, Indian airlines are about to take off to new heights.