Unveiling the Downside of Market Timing

By Nilesh Naik, Head of Investment Products, Share.Market (PhonePe Wealth)

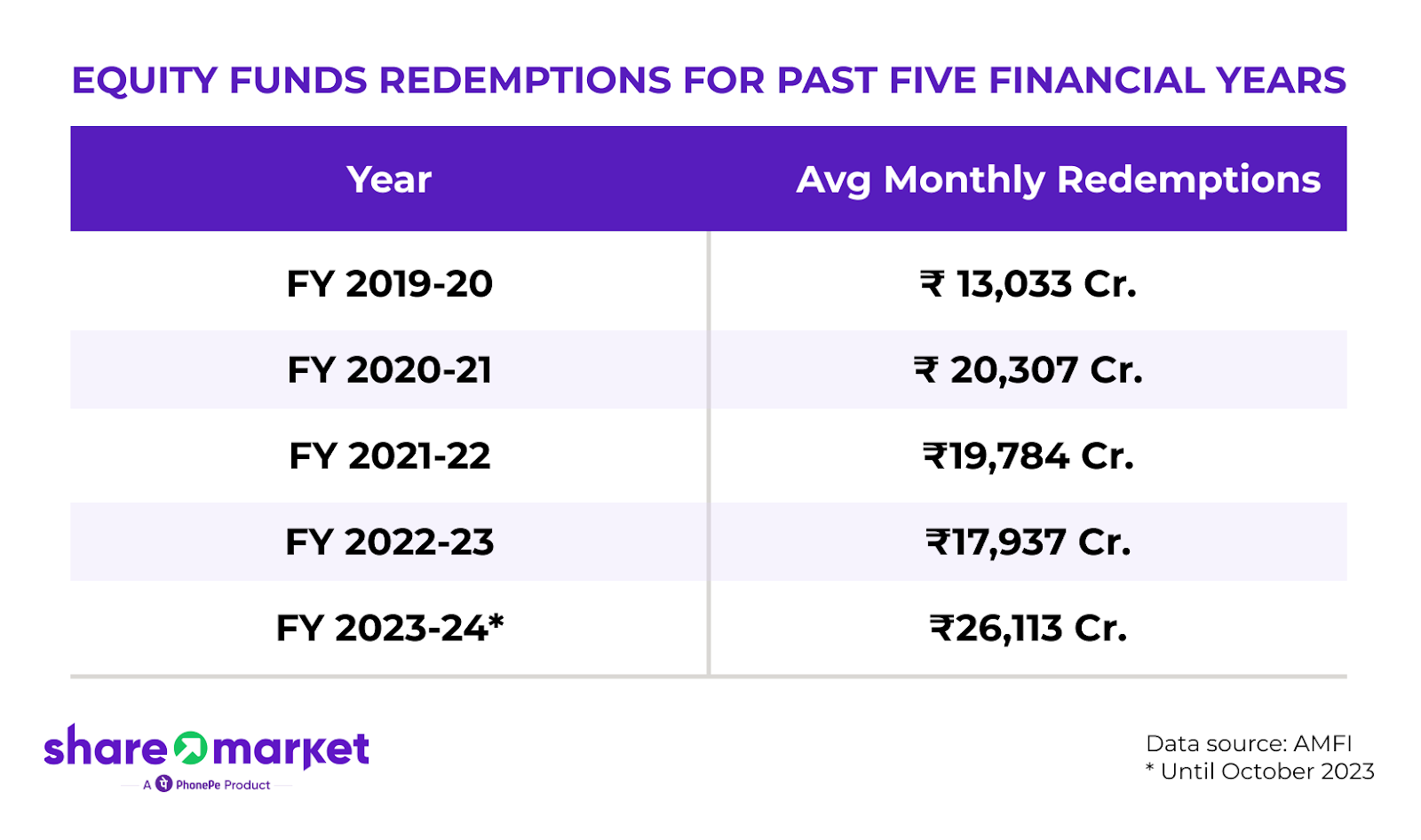

In the financial year 2023-24 so far, monthly redemptions from equity funds have averaged about ₹ 26,100 crore, a jump of 46% over the previous financial year when average monthly redemptions were about ₹ 17,900 crore. All-time high market levels and a significant market recovery after the correction in the second half of the financial year 2022-23 could be some of the key reasons for such increased redemptions. In other words, equity fund investors seem to be trying to time the market in the pursuit of better investment results.

But does such behavior of timing the market really yield better investment results?

Over the years, we have observed that investors’ decisions to enter or exit the market are often driven by emotions and behavioral biases instead of being pragmatic. For e.g. Whenever there has been a big market fall or a sluggish market phase (2008, 2011-13, 2020, etc.), the inflows in equity funds reduce significantly and vice versa. Likewise, a recovery after a market fall has often coincided with increased redemptions, which is a classic behavioral bias called “disposition effect”.

Thus such attempts to time the market often work against the interests of investors rather than helping them achieve better investment results. In fact, investors who hold on to their investments for a long term tend to do far better than most investors who attempt market timing. As Warren Buffet once said “Much success can be attributed to inactivity. Most investors cannot resist the temptation to constantly buy and sell.”

But what exactly is the downside when investors fail while trying to time the market?

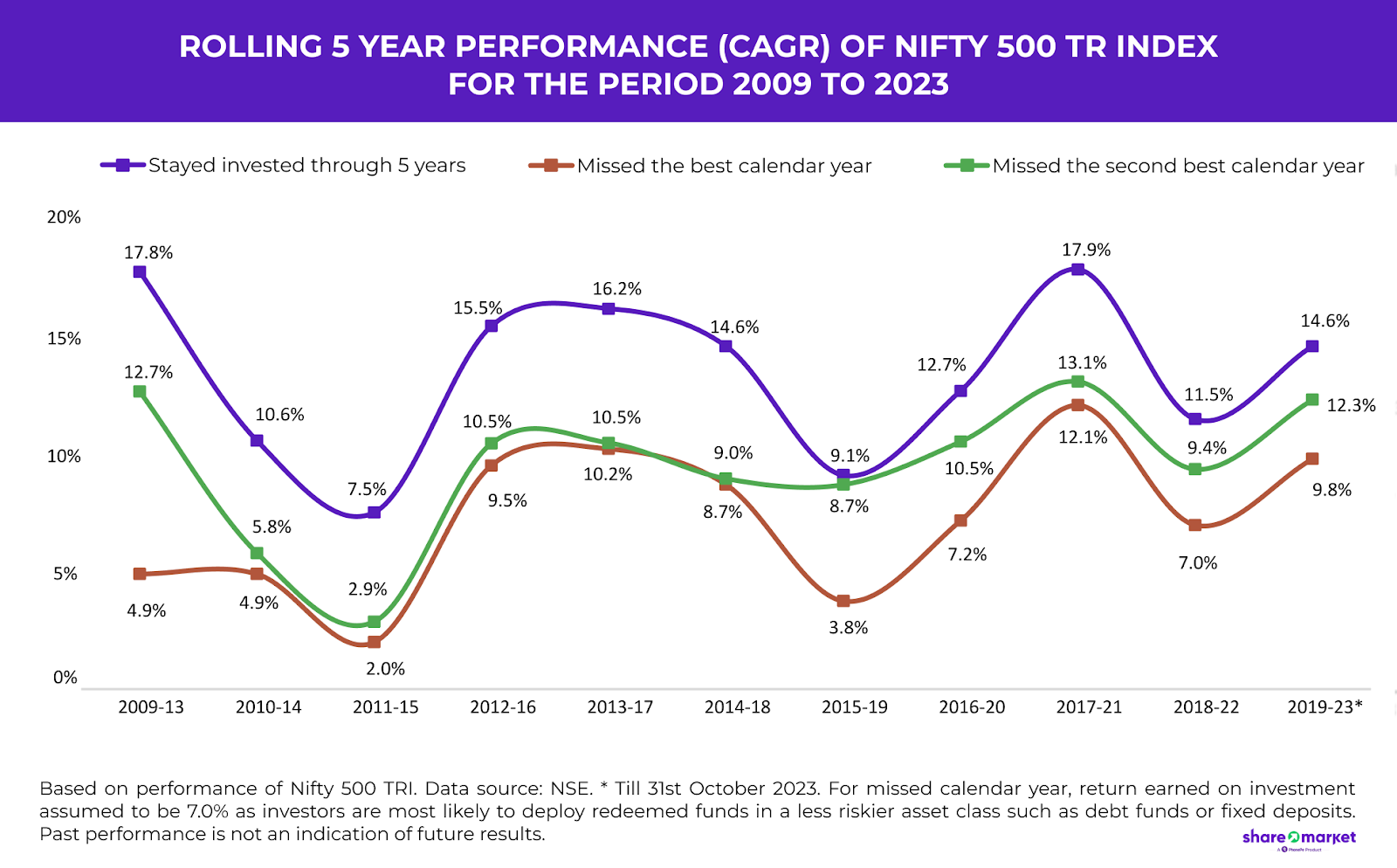

To assess this impact, we first looked at the rolling 5-year performance in the market (Nifty 500 TRI) at the end of each calendar year, over the past 15 years. We then calculated the performance during each of those 5-year periods assuming the investor ends up staying out of the market in the best performing calendar year during that 5-year period. Further, we also calculated the impact if the investor misses the second best performing calendar year. Since investors who exit their equity investments are likely to deploy it in some other low risk asset such as debt funds or fixed deposits, we have assumed that the investor would earn a 7% return in the year they stay out. The findings of this analysis are presented in the graph below.

As can be seen in the graph above, for the period 2009 to 2013, the annualized return of the Nifty 500 TR Index was 17.8%. But if the investor had missed the best year during this period, the annualized return would have dropped to 4.9% – a difference of 12.9%. Likewise, for the period 2017 to 2021, the annualized return of Nifty 500 TR Index was 17.9% vs 12.1% if the investor had missed the best year – a difference of 5.8%. On an average this difference in 5-year CAGR between “stayed invested for 5 year period” vs “missed best year” has been 6.2% over the past 15 years. Even if the investor had missed the second best year, the annualized 5-year return would have been lower by 3.9% on an average as compared to staying invested for the 5 year period. Massive, isn’t it?

So how can investors overcome this problem?

The best way to address this issue is to follow an asset allocation approach instead of trying to time the market based on emotions or behavioral biases. This can be broadly done in two ways:

- Static asset allocation approach: In this approach, an investor can arrive at an appropriate asset allocation based on his investment objectives, investment horizon, risk tolerance, etc. Once the asset allocation is decided, it becomes easy to make buy / redeem decisions. For eg, if the stock market goes up significantly leading to substantially higher equity allocation in an investor’s portfolio compared to what’s been decided, a portion of equity assets can be redeemed to revert to original asset allocation and vice versa.

- Dynamic asset allocation approach: Informed investors who want to to be more dynamic in their asset allocation by adding market related parameters such as market valuations to decide their asset allocation can follow this approach. However, when investors opt for this approach, it is important to follow a robust process in a disciplined manner rather than allowing your emotions or behavioral biases to impact your decisions.

Investors should take the approach that best suits their investment expertise, financial goals, and risk tolerance. Investors should be aware that allocation approaches that involve reacting to market movements requires in-depth understanding and expertise of the market. Perfectly timing the market is next to impossible, so make sure your strategy is not vulnerable to arbitrary errors.

PhonePeWealth Broking Private Limited is a member of NSE & BSE with SEBI Regn. No.: INZ000302639,

Depository Participant of CDSL Depository with SEBI Regn. No.: IN-DP-696-2022 and ARN- 187821. Member id : BSE – 6756 NSE 90226. PPWB acts as a distributor of Mutual Fund and WealthBaskets. Investments in the securities market are subject to market risks, read all the related documents. This content is exclusively for educational and informational purposes only. Disputes with respect to the distribution activity would not have access to Exchange investor redressal or Arbitration mechanism.