The Future of Investment Strategies: Analyst Sentiment Factor Uncovers a New Wave in Quant Investing

- Share.Market

- 5 min read

- 15 Apr 2024

By Vaibhav Jain, Head of Content and Education, Share.Market

The world of tech is crazy. With each passing month, we have new releases of innovative screen folding phones, doctor-replacing smartwatches, and eye-opening mixed reality headsets (literally). It’s difficult to keep up with it.

That’s where tech reviewers give their valued opinions on different varieties of tech launched to help customers decide whether it’s good for them.

While their opinions can be biased or lack nuance, it wouldn’t be wrong for us to conclude that an aggregation of the opinions of many reviewers can take us in the right direction.

This is not limited to tech, but rather true for life in general. Everybody can’t be an expert at everything.

But why are we talking about tech, being investors?

Because investing is no different. In the world of stock markets, there are analysts who are equivalent to a reviewer in the tech products world, who give their opinions on stocks, because they are good at it and spend hours studying them.

Does this mean we should listen to these analysts? Some might argue that they don’t add any value to the stock research. But let’s not dismiss them altogether, because if they were totally useless, they wouldn’t continue to exist for this long.

They can come in handy to those who understand how to yield their power.

In the stock market, an analyst’s advice can be harnessed by a gleaning analyst sentiment factor, a data and quant-driven layer that gives a forward-looking view of the capital markets.

Enter – Analyst Sentiment factor!

Do these 3 words actually mean something?

Don’t worry. They are not an output of a random 3-word generator software. Rather, they are a key to possible alpha generation in the markets – at least, that’s what many academic research shows.

To understand what they mean, let’s take a small step back.

As described earlier, analysts are those stock experts who give their opinion on the stocks they study. During their study, they make fair estimates of how the business will do over the foreseeable future. As time passes – as it does – with the normal course of business, the company announces updated information about how they are doing, and analysts get to work again.

They revisit their opinions on the stock they had earlier shared and then input the new information about the stock to fine-tune their models and come up with new estimates of how they think the business should do. These estimates undergo what we call “revisions.” These revisions can be positive or negative based on the new developments and analyst’s studies.

When these revisions happen, the price of the stock witnesses a knee-jerk reaction. Positive revisions lead to price increases and vice versa.

But, here’s the key part: markets often underestimate the “subtle aspects of the revision”, therefore originating a lag between analyst revisions and their true impact on the stock price. While the impact could have been more intense, markets are not able to absorb these revisions as quickly as we might think they do.

And here the Analyst Sentiment factor comes into play.

To technically define this factor – The analyst sentiment factor measures changes in analyst expectations of a company’s future performance based on revisions made to the financial outlook or price targets.

And when we aggregate the expectations of all the analysts in the market into a score, and rank stocks based on which stocks have the most positive revision in their analyst expectations, we can come up with a portfolio with higher chances of alpha generation.

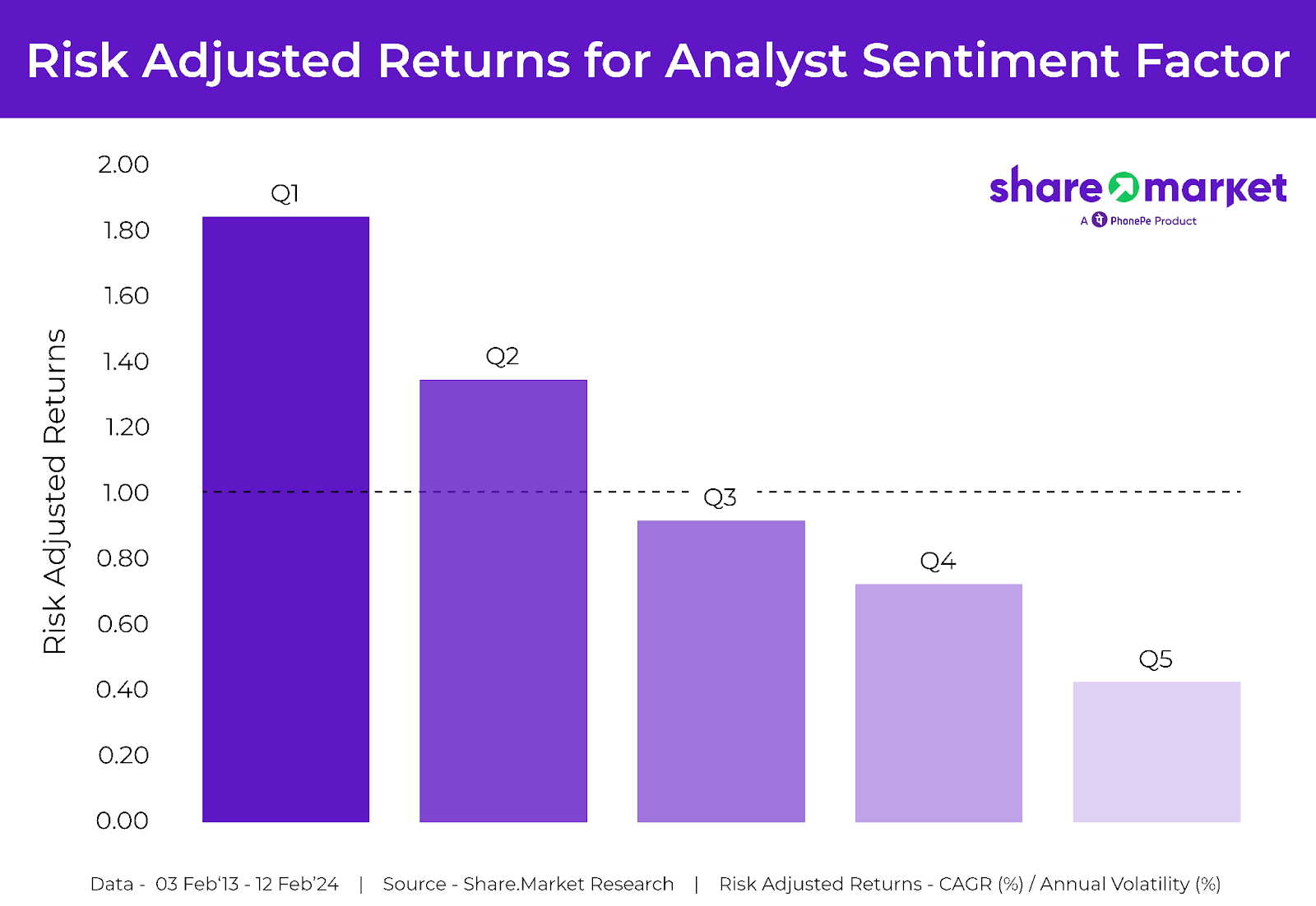

Case in point, here is what happened when we took the Analyst Sentiment factor, scored and ranked stocks based on it, and then compared the Risk-Adjusted Returns (CAGR / Annual Volatility) of different quintiles, where Q1 consisted of the top 20% portfolio of stocks with the highest positive analyst estimate revision while Q5 had the bottom 20% stocks with most negative analyst revision.

Note: Risk-adjusted returns are factual, shown for information purposes only, and not as an advertisement/promotion or as an assurance of future returns. Past performance does not guarantee future returns.

The results proved our hypothesis. Stocks with positive analyst estimate revisions perform better than stocks with negative revisions.

Bringing it home

Though traditional factors like momentum, value, and low volatility have become mainstream in India, they still offer a huge potential for early investors to leverage for elevated investment performance. More nuanced factors like Analyst Sentiment as discussed above, which still remain under the radar, are positioned to be of even greater use to investors.

This article was originally published in Economic Times on 18-03-2024

Disclaimer

Investments in securities are subject to market risks. Read all the related documents carefully before investing.

All investors are advised to conduct their own independent research into investment strategies before making an investment decision.

PhonePeWealth Broking Private Limited is a member of NSE & BSE with SEBI Regn. No.: INZ000302639, Registered Office Address: Office – 2, Floor 3, Wing A, Block A, Salarpuria Softzone, Bellandur Village, Varthur Hobli, Outer Ring Road, Bangalore South, Bangalore, Karnataka – 560103, Depository Participant of CDSL Depository with SEBI Regn. No.: IN-DP-696-2022, Research Analyst– INH000013387 and ARN- 187821. Member id: BSE – 6756 NSE 90226. CIN U65990KA2021PTC146954. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

This article is for educational purposes and should not be considered as a recommendation.