Taking a step beyond RBI’s inflation rate for your financial planning

By Vaibhav Jain, Head of Content & Education, Share.Market (PhonePe Wealth)

Inflation numbers for November 2023 are here and there are reasons to be happy about it. Although the retail inflation number surged slightly to 5.55% (from 4.87% in October), it is still within RBI’s tolerance band of 2-6%.

That means, on average, goods and services have gotten 5.55% more expensive compared to November 2022.

But there’s a huge problem with the above statement. While things have gotten expensive by 5.55% “on average”, that might not be the case for you, as an individual or household.

The problem with averages is that they do a good job of explaining observations for a population, but when an individual uses the same averages to make decisions, it can lead to dangerous outcomes.

This inflation number is representative of an extremely diverse India. India that lives in both skyscrapers & slums. India that eats in roadside dhaabas & Michelin star restaurants. India that shops from Gucci & Palika Bazaar.

And then there is you, who might lie somewhere in the middle. Now, you can only imagine if you start taking the inflation number seriously when building your financial plan. It will be a disaster. Afterall, it’s YOUR financial plan, not an average Indian’s.

So what do we do? Do we simply ignore this arbitrary number called inflation?

That wouldn’t be a great decision either. That’s why you should learn to calculate the inflation rate for yourself. That’s what we will do here – in the simplest way possible.

To start with, we don’t have to take out our spreadsheets and start calculating how much our bread price increased since last year. The Ministry of Statistics & Programme Implementation (MoSPI) does this for us.

So, we will build on that.

MoSPI gives us index values for each basket of goods (Pulses, Vegetables, Clothing, Housing etc.) for each month which helps us in computing inflation that happened for that specific good.

Then it also assigns different weights to each of these categories based on what it deems representative of how an average India spends its money.

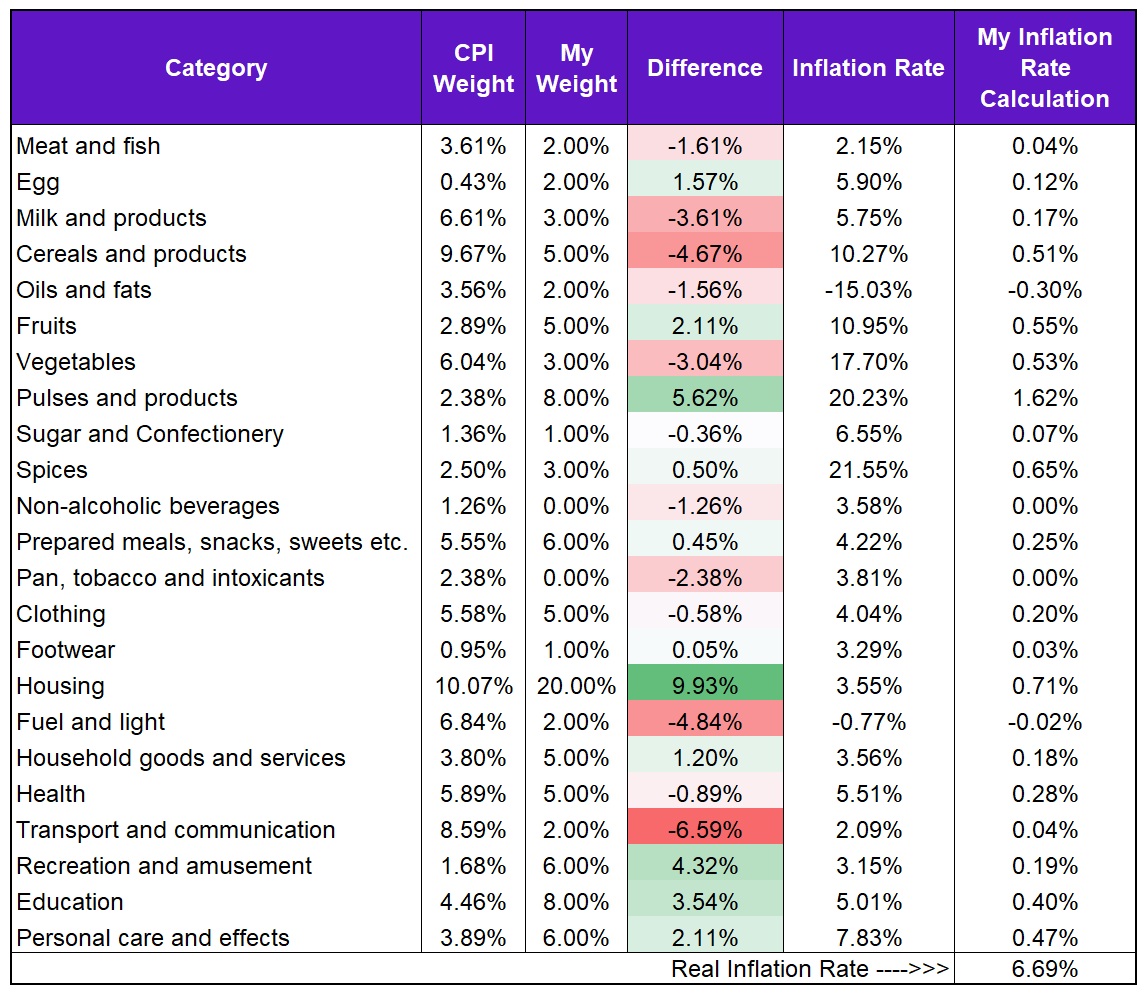

This is what it looks like for November 2023.

Source: MoSPI

When computing YOUR inflation rate, you can start by first finding in what ratios you end up spending money across these categories.

While an average Indian may be spending 2.38% of their expense budget on Pan, tobacco and intoxicants, it can be 0% for you. Similarly, 1.68% spent on Recreation and amusement doesn’t really explain the spending habit of a 20-something young adult who loves partying on weekends. Also, you could be vegan, and therefore spending 10.65% of your budget on meat, fish, egg & dairy products would be a misrepresentation of your expenses.

So, take out your pen and paper (or better, spreadsheet) and chart a budget of what your spending looks like. This will be a very messy exercise, since it’s always difficult to keep close track of where your money is going. But, this one time exercise will not only help you find your inflation number, but also help you with saving more.

Subsequently, observe the difference between what an average India spending habits compare to yours. Finally, multiply your weights with the inflation rate and add them together.

Let’s take an example of, say, my personal consumption of various products.

Voila, here’s your inflation rate.

You can customize it further, by taking index values and inflation rate of these categories for only Rural or Urban, which better explains your situation. I used combined numbers for ease of calculation.

PhonePe Wealth Broking Private Limited is a member of NSE & BSE with SEBI Regn. No.: INZ000302639, Depository Participant of CDSL Depository with SEBI Regn. No.: IN-DP-696-2022 , RA SEBI Reg. No. :INH000013387 and Mutual Fund distributor with AMFI Registration No: ARN- 187821. Member id : BSE – 6756 NSE 90226.

Investments in the securities market are subject to market risks, read all the related documents.

This article was originally published in The Economic Times on 15-12-2023