Mid and small-cap indices did great in 2023, but which ones are the best?

A meta-analysis of the seven major indices tracking mid and small-cap space in the Indian markets

By Vaibhav Jain, Share.Market Research

I. Introduction

2023 was a year of Indian equities as an asset class, but more so for mid and small caps. Despite the volatility of international uncertainty and geopolitical tensions, Indian markets stood strong. While Nifty 50 returned 20%, mid and small caps were in excess of 40%.

The year of the bulls, 2023 was marked by stabilized interest rates and heavy government PLI schemes, among other macroeconomic factors. More importantly, the disproportionate amount of net inflows pumped into these stocks by the domestic mutual funds industry is astounding.

The last year began with large-cap funds receiving the most inflows, but the tide turned in favor of smaller companies pretty quickly. Coupled with the greater inflows in small caps and the low float of these companies, we get a deadly combination of P/E expansion. Because more money chases the fewer available stocks, prices shoot up on the back of increased P/E.

Case in point – Nifty Smallcap 250 P/E expanded from 19.04 to 27.37 in the last year. This means that of the ~49.1% return that the index gave, ~43.8% of it came from P/E expansion only.

While years like 2023 highlight how great mid/small-cap exposure can be in your portfolio, we can also fall prey to being myopic in our decision-making. After all, your investment portfolio is meant to serve you for years, if not decades, and making changes based on just the past year’s performance can be foolish.

Therefore, we decided to conduct this meta-analysis on the mid/small-cap space, taking data back to April 2005, spread across 7 different indices in this space for metrics across risk and return. Our goal is to provide a more comprehensive outlook so that you can make smarter decisions for your portfolio in 2024.

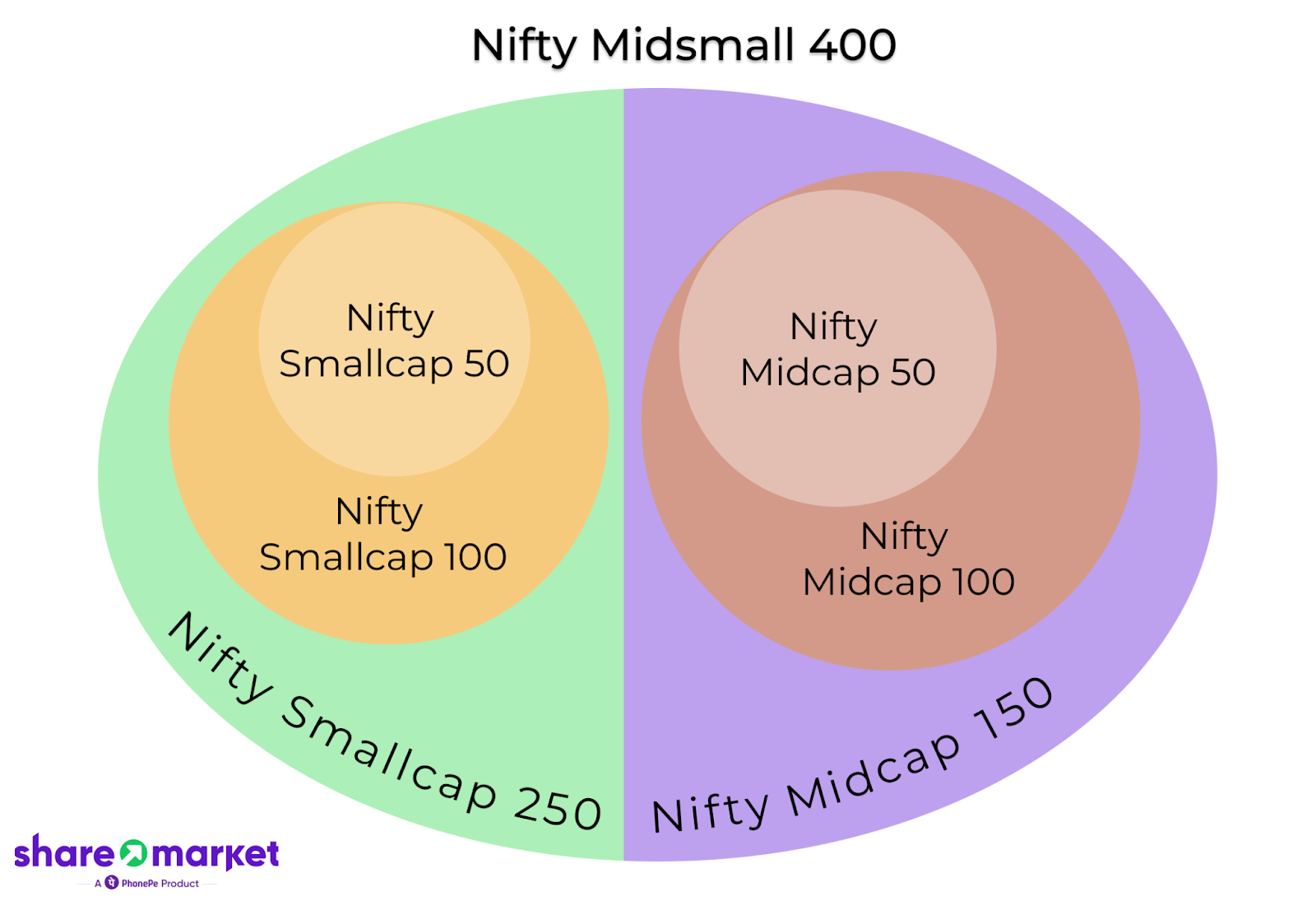

II. Understanding the Indices

Let’s start by breaking down the technical definitions of the seven Nifty indices we’re analyzing:

- Nifty Midcap 50 – Top 50 companies based on market cap from Nifty Midcap 150 index

- Nifty Midcap 100 – Comprising Nifty Midcap 50 and the remaining companies based on average daily turnover from Nifty Midcap 150

- Nifty Midcap 150 – Companies ranked 101 to 250 based on full market cap

- Nifty Smallcap 50 – Top 50 companies based on average daily turnover from top 100 companies selected based on full market cap in Nifty Smallcap 250

- Nifty Smallcap 100 – Consisting of Nifty Smallcap 50 and the remaining companies selected based on average daily turnover from the top 150 companies in Nifty Smallcap 250

- Nifty Smallcap 250 – Companies ranked 251 to 500 based on full market cap

- Nifty Midsmall 400 – A union of Nifty Midcap 150 and Nifty Smallcap 250

In simpler terms, imagine Nifty Midcap 50/100 & Smallcap 50/100 as subsets of Nifty Midcap 150 & Smallcap 250 respectively, while Nifty Midsmall 400 is a combination of Nifty Midcap 150 & Smallcap 250. Refer below image for a better understanding.

Our goal in this study is to investigate where each of these indices stand based on their risk and return metrics.

Note: For the purpose of this analysis, historic values of the Total Return Index have been taken from NSE. Past performance of the indices is neither an indicator nor a guarantee of future performance, and may not be considered as the basis for future investment decisions.

III. Return Analysis

CAGR Analysis: Unveiling the Winners

Commencing with a fundamental comparison of Compound Annual Growth Rates (CAGR) from April 1, 2005, to December 31, 2023, the results present a fascinating narrative:

Observations:

- Contrary to the anticipation that more concentrated indices perform better, larger counterparts outshone them. The conventional wisdom of “Over diversification reduces the magnitude of gains” faces a challenge this time.

- Surprisingly, a bird’s-eye view reveals that Midcap indices outperformed Smallcap indices, challenging the notion that smaller companies should yield superior returns.

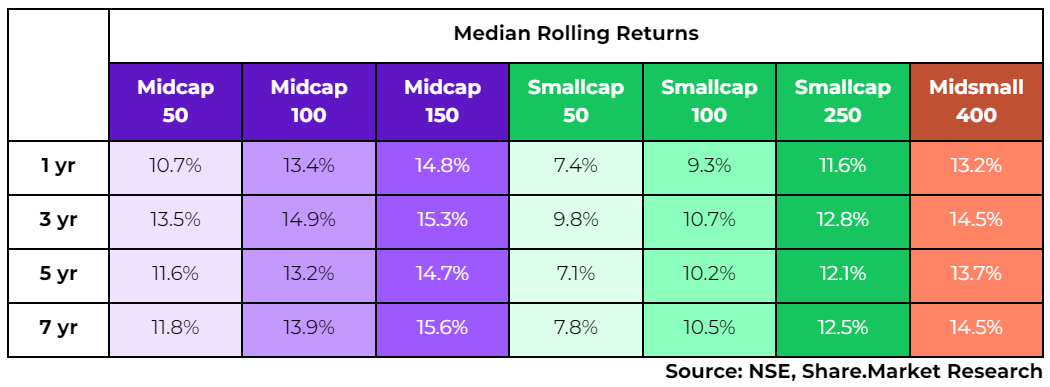

Rolling Returns: A Deeper Dive

However, relying solely on point-to-point returns can be misleading. A dive into median rolling returns over 1, 3, 5, and 7-year periods across the 18 years provides a nuanced perspective.

What are rolling returns? – It is a way of measuring the performance of the index over various overlapping periods. Instead of looking at the total return over a fixed period, rolling returns provide a series of returns for different, contiguous periods (1, 3, 5 & 7 yr) of the same length.

The results align with our earlier findings:

The story remains consistent: Midcap indices outperform Smallcap, and larger indices consistently beat their smaller counterparts.

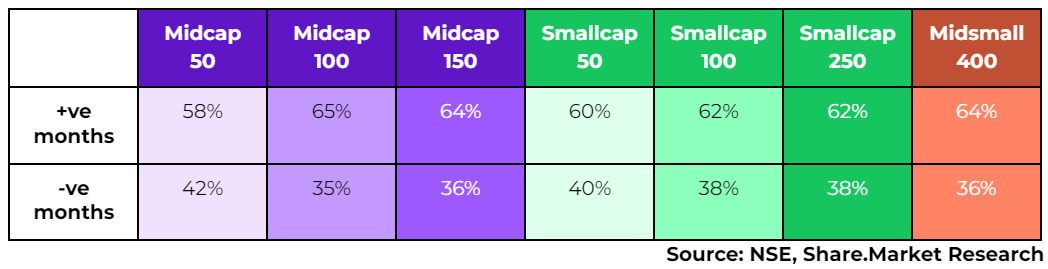

Monthly Returns: The Short-Term Rollercoaster

Taking a step further, let’s delve into the returns on a monthly basis across the 226 months of our research period. Here’s a snapshot of what investors’ returns would look like if they invested their money for a single month:

Observations:

While a month may seem too short for conclusive judgments, Smallcap 50, stands out with subpar median returns indicating higher volatility without adequate compensation.

Additionally, the percentage of months with negative returns for each index further underscores the challenges faced by smaller indices:

Building upon previous observations, smaller indices consistently disappoint investors more frequently, with a higher likelihood of negative returns. In contrast, the superset index, Midsmall 400, demonstrates a 64% chance of ending the month positively.

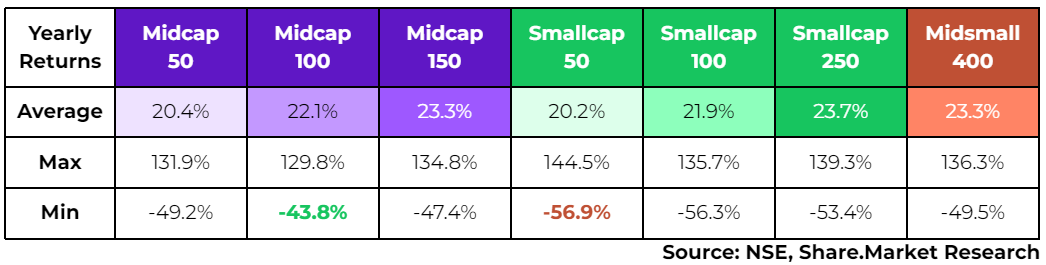

Yearly Returns: Closer Look

Repeating the in-depth analysis for yearly returns provides further insights into the performance of each index:

Observations:

- Notably, Smallcap 50 exhibit the highest and lowest returns, emphasizing its volatile nature. Investors in Smallcap 50 should be prepared for significant fluctuations in yearly returns.

- Surprisingly, Midcap 100 surprises by displaying the least minimum returns in a financial year. This suggests fair consistency in returns, making it an interesting index for investors seeking stability.

- Midcap 150, Smallcap 250, and Midsmall 400 maintain their positions as the top three performers in terms of average annual returns. This aligns with the trends observed in monthly returns.

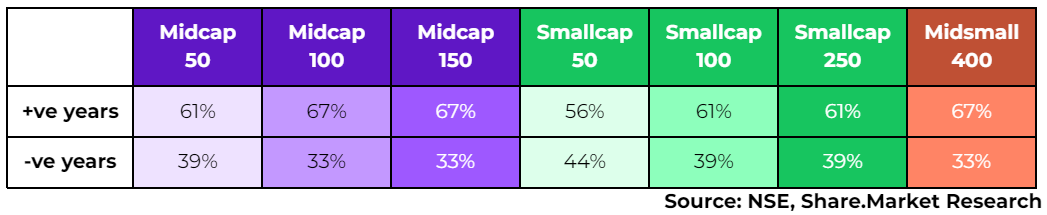

Moreover, we investigated the % of years with negative returns for each index:

Midsmall 400, Midcap 150, and Midcap 100 exhibit a high probability of 2/3rd for an investor to experience positive returns, reinforcing previously observed conclusions.

Interestingly, when comparing the percentage probability of positive returns for the same index between monthly and yearly data, the latter consistently shows higher chances of positive returns. This underscores the idea that expanding the investment horizon across any asset class or index increases the likelihood of avoiding losses.

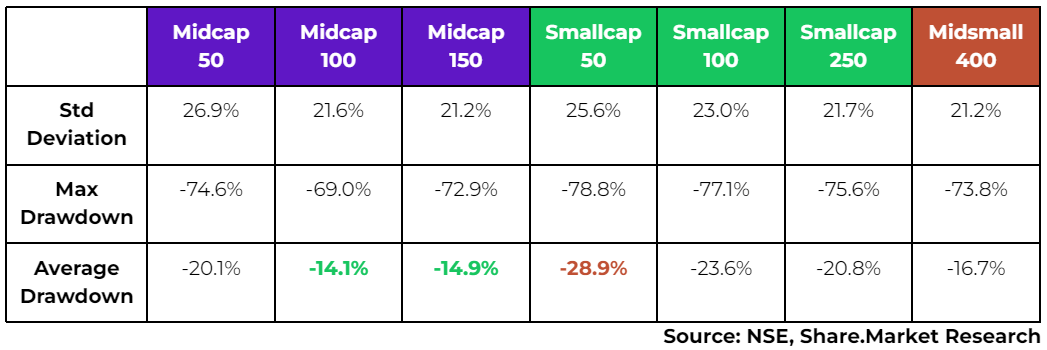

IV. Risk Analysis

Half-knowledge is always dangerous. In every sphere of life. Talking about returns without emphasizing the risk is a poor job done by an investor. But we will not commit this sin. We will also try to cover all possible areas of risk that one must be aware of these indices.

Observations:

Standard Deviation: This measures how much daily returns deviate from the average. Higher values indicate more volatility and, consequently, a riskier investment. Larger indices exhibit promising signs of lower standard deviation compared to their smaller counterparts.

Drawdown: It signifies the percentage drop in an index from its previous all-time high. Maximum drawdown represents the maximum percentage decrease before recovery, while average drawdown provides an average of such drops. Smallcap 50 shows the highest figures, indicating potentially heavier intermittent losses. In contrast, Midcap 100 and 150 demonstrate resilience, experiencing lower drawdowns.

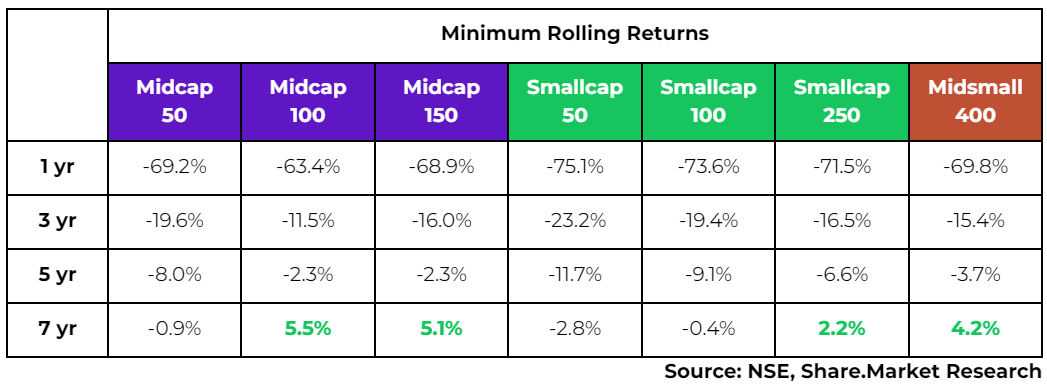

Expanding our analysis from the previous section, we take a closer look at rolling returns. Rather than focusing on median returns, we shift our attention to computing the minimum returns an investor might have encountered over 1, 3, 5, and 7-year investment periods:

The small and midcap space is notorious for prolonged periods of negative performance. While large-cap indices typically recover within 3-5 years, small and midcaps might take up to 7 years to turn positive. Midcap 150, Midcap 100, Smallcap 250, and Midsmall 400 exhibit quicker recovery periods, making them appealing choices for investors seeking resilience in the face of drawdowns, breaking even in year 7 in the worst-case scenario.

By combining insights from this table with the previous one, we can identify indices that:

- not only experience lower drawdowns

- but also exhibit quicker recovery.

Midcap 150, Midcap 100 & Midsmall 400 meet these criteria.

V. Crisis Response

An investment is only as good as your commitment to it. You can identify the best investment opportunity of the decade, but if you do not hold it for the whole decade, you are as average as the next-door investor. Conviction and patience are often put to the test during a crisis, leading many to sell due to the unbearable short-term losses. It’s a human response, but it can significantly impact long-term gains.

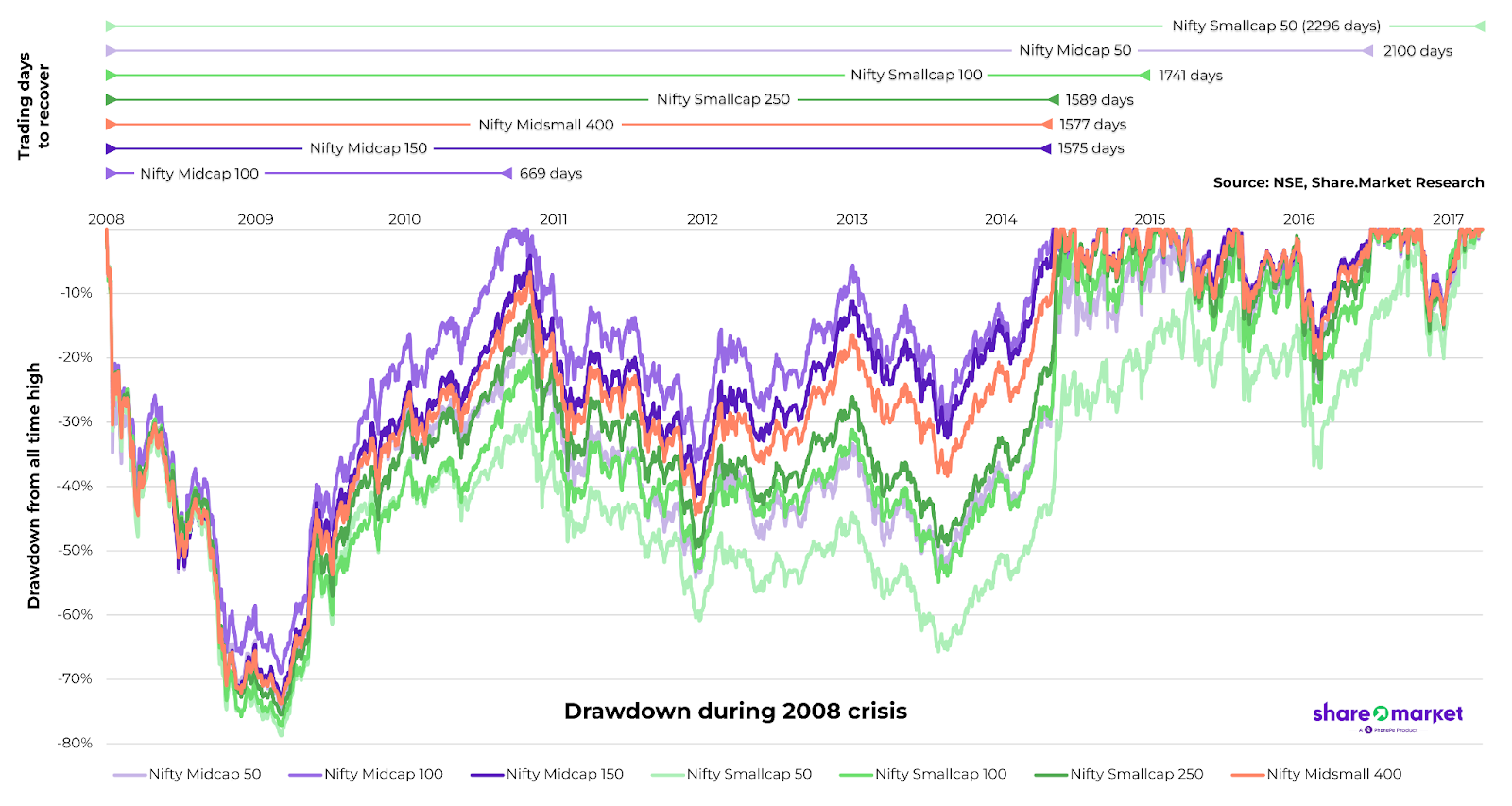

Before concluding our analysis, we take a crucial detour to stress test our indices and evaluate their performance during a crisis. While the memory of the recent COVID crash is still vivid, we choose to navigate back to the 2008 subprime crisis for a more rigorous examination.

Unlike the liquidity-fueled anomalies of the COVID era, the 2008 crisis provides a clearer lens to understand the true nature of these indices.

Here is what we found:

The markets hit their peak on 07 Jan ’08, initiating a downward spiral that persisted until early 2009. During this carnage, all indices experienced a synchronized decline, with the Midcap 100 offering a relative sense of relief.

As the market bottomed, the difference between Midcap 100 and Smallcap 50 was ~10%, with the former falling less. The performance divergence among indices became apparent when recovery started.

Upon recovery, the gap widened, and Midcap indices, led by Midcap 100, ascended more swiftly than their Smallcap counterparts. Surprisingly, Midcap 100 breached its previous high within 669 days, maintaining its supremacy during crises.

All this while, the rest of the Smallcap indices and Midcap 50 further continued to lag in performance only increasing the gap between them and top performers.

The relief in the markets post-2014 marked the resurgence of the Midcap 150, Midsmall 400, and Smallcap 250, finally breaching their all-time highs. In contrast, Midcap 50 and Smallcap 50 took until Jul ’16 and Mar ’17, respectively, to recover.

Observations:

- Smallcap/Midcap 50 indices took roughly a decade to recover from previous highs.

- Midcap 100, Midcap 150, Midsmall 400, and Smallcap 250 displayed quicker recovery.

- Smallcaps, in general, lagged behind Midcaps, with Smallmid closely following the path of Midcaps.

VI. Conclusion

All this analysis means nothing if investors like yourselves cannot take action on it. So here is a summary of our findings in a few words:

“Throughout the risk and return spectrum, a prevailing trend emerges: midcap indices consistently outperform small-cap indices, while larger indices surpass their more concentrated counterparts.”

Hence, when considering asset allocation, incorporating a portion of mid-cap leaning passive products can be a prudent strategy for investors exploring opportunities in the mid and small-cap space, based on the above analysis.

Note that the above conclusions and analysis hold true primarily for investors following a passive investment strategy. If you plan to explore actively managed mutual funds in this space, the conclusions may vary based on the specific fund manager’s strategy and performance which is outside the purview of this study.

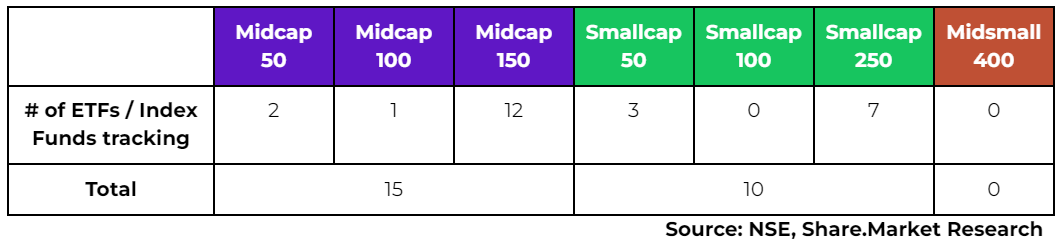

This also aligns with the current landscape of the mutual fund industry, where midcap indices have a higher number of ETFs and index funds tracking their portfolios compared to small-cap indices. While our analysis suggests that midcap indices consistently outperform small-cap indices, it’s important to note that this could be one of the many factors influencing the fund offerings.

Notably, the Midsmall 400 index, despite its promising characteristics, currently lacks representation through ETFs/Index Funds.

Ultimately, our analysis aims to empower investors with actionable insights, allowing them to make informed decisions in aligning their investment strategies with the observed trends in the market. We compiled these observed trends in this article. It is your time to take action for your portfolio!

For general educational purposes only and should not be construed as advice.

PhonePeWealth Broking Private Limited is a member of NSE & BSE with SEBI Regn. No.: INZ000302639, Depository Participant of CDSL Depository with SEBI Regn. No.: IN-DP-696-2022, Research Analyst – INH000013387 and Mutual Fund distributor with AMFI Registration No: ARN- 187821. Member id : BSE – 6756 NSE 90226. CIN – U65990KA2021PTC146954.

Investments in securities market are subject to market risks, read all the related documents carefully before investing.

Registration granted by SEBI, and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

This article was originally published at Economic Times on 27-01-2024